Top Financial Planning Tips for 2014

Marin Mommies presents a guest article by Marin mom and financial planner Tanya Steinhofer, CFA,CFP®.

Marin Mommies presents a guest article by Marin mom and financial planner Tanya Steinhofer, CFA,CFP®.

Below is my attempt at a Top 10 List of Financial Planning Tips for 2014. Some of the items are things you should try to do every year, while some are unique to the current period and what we’ve gone through over the past few years. This is a compilation of ideas gathered from others as well as a few of my own.

- Invest in yourself. You are your largest asset and so it pays to take care of yourself. Your human capital is your largest asset so make sure you are on the right career path. If not, hire a career coach or consider additional education. Also, eat well, exercise and laugh more!

- Evaluate whether a Roth IRA conversion might make sense. This strategy is particularly relevant for the young, those who can pay the taxes with outside assets, those who expect to be in a higher tax bracket in retirement and those who would like to pass their IRA on to heirs.

- Be flexible. The markets are likely to remain volatile for some time and may not deliver stellar returns, so we all need to be flexible in our plans and may need to accept an alternate scenario.

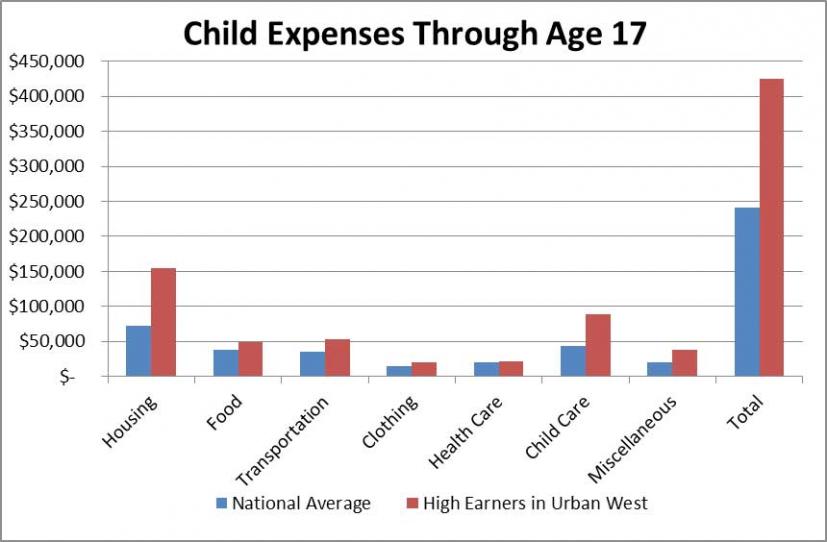

- Live within your means. Even though the economy is improving, many people are still recovering from the effects of un- or under-employment. Keep your expenses low as your income improves so you can save more for your future goals and get back on track.

- Review your employee benefits. Many firms have begun offering Roth 401ks and Health Savings Accounts (HSAs) over the past few years. Also explore whether you can set aside pre-tax dollars to pay for childcare expenses. Consider these opportunities if available.

- Pay yourself first. No one else is going to pay for your retirement, so be sure to make regular contributions to your 401k or IRA. Be sure to at least contribute as much as any employer match so as to not leave free money on the table. Automatic paycheck withdrawals make it easy to contribute.

- Chase yield (carefully). With most cash investments yielding under 1%, leaving extra money in cash is not a wise choice. With money not earmarked for short-term uses or emergency savings, consider extending the maturity into the one- to three-year range (e.g., with a short-term bond fund).

- Rebalance (or review) regularly. One of the lessons from 2009 is that it is particularly dangerous to attempt to time the market, as those who bailed in March only to watch the market climb for the rest of the year found out. A smarter strategy is to stay invested and rebalance your portfolio any time your allocations to specific asset classes (e.g., stocks, bonds, real estate) are more than 10% above or below the desired target percentages. Using a range will allow asset classes that are in a bull market time to run without cutting them back too soon, while waiting to buy beaten down asset classes until they are really inexpensive.

- Review your estate plan documents. Given all the changes in the estate plan laws in the past year, chances are good that your living trust needs to be updated. If you haven’t yet drafted estate plan documents and have young children, put it high on your priority list to do in 2014.

- Keep an eye on fees and expenses. Without strong economic growth to drive the stock market, future returns are likely to be sub-par. This outlook increases the importance of minimizing investment expenses. Pay attention to the commissions, fund management and other expenses incurred on your investments.

Tanya Steinhofer, CFA, CFP® is an independent, fee-only financial planner helping busy families achieve financial peace of mind by exploring and integrating their dreams into their financial roadmap. She offers comprehensive financial planning, but doesn’t manage assets so there are no account minimums to worry about. She lives in Mill Valley with her husband and two young children. She can be contacted at tanya@redwoodgrovewm.com or you can visit her website at www.redwoodgrovewm.com.